For your team

Migrate to Skyone

Featured products

Ecosystem and collaboration

Risk-based financing: what it is, how it works, and what the benefits are

If you're diving into the world of finance or simply looking to expand your knowledge of investing, it's essential to understand what withdrawal risk and how it can influence your financial decisions.

This operation is a type of receivables financing where a company sells its future credits, originating from sales on credit, to a financial institution. This allows the company to immediately the financial resources it would expect to receive in the future, optimizing its cash flow and reducing the waiting time for payments from its customers.

According to data from Citi , the practice of discounting accounts is growing among large retailers since 2020. They show that this type of operation has accounted for R$ 3.9 billion of the total R$ 8.6 billion in accounts payable to suppliers for Magazine Luiza, and R$ 2.5 billion of the total R$ 9.6 billion for Via Varejo, for example.

Therefore, throughout this article, we will cover all aspects behind the concept of risk-taking , from its definition to its practical application in financial markets. Furthermore, we will explore the different types of risks involved, strategies for mitigating them, and the advantages of adopting this approach in your investment portfolio.

Stay with us!

The term "risk discount" refers to a financial practice within the business context where a financial institution advances funds to a company, the supplier , related to sales made on credit.

This operation is commonly used in the market to improve the cash flow of suppliers who do not wish to, or cannot, wait for the payment deadline from their customers, known as debtors .

In order for suppliers to participate in these receivables financing operations, they generally assign to the bank the credit rights they would have with the debtor. Thus, the financial institution assumes the credit risk related to non-payment by the debtor, a condition that justifies the name of the operation.

In summary, the factoring mechanism relieves the supplier of liquidity pressure and the risk of default, transforming sales on credit into immediate capital available for investments or current expenses.

What is its importance in the current financial context?

The risk-draft facility emerges as a relevant alternative in the current financial market, especially in our scenario of economic volatility . As we have seen, by offering financing to companies seeking working capital, it becomes vital to the financial health of organizations by providing immediate liquidity.

Financial institutions such as banks play a key role in providing down payment risk, assuming the credit risk arising from commercial transactions. The importance of these operations is reflected in their contribution to the stability and growth of companies, while maintaining the flow of active capital in the market.

Using factoring implies, for the financial institution, a careful credit assessment and often establishes a closer relationship with the client. This arrangement finances medium- to long-term operations and is mostly related to debt instruments such as bills of exchange or promissory notes.

Therefore, factoring is an increasingly important tool in the financial ecosystem, helping companies overcome difficulties and allowing banks to diversify their credit operations.

How does risk-taking work?

The risk-sharing mechanism is a financial tool that has brought several benefits to companies and suppliers. See below how each step of this process works:

Invoice issuance

In the initial stage, the supplying company issues an invoice for the product or service provided and sends it to the customer.

Advance agreement

The parties involved establish a formal agreement for the anticipation of receivables, defining prior terms and conditions for the transaction, such as interest rates and payment deadlines.

Request for advance payment

The supplier company then requests an advance payment of the invoice amount from a financial institution or the client, who agrees to make the advance payment.

Credit analysis

The financial institution conducts a financial analysis, evaluating the creditworthiness of the supplier and the viability of the asset risk.

Release of funds

Once the transaction is approved, the funds are released. The financial institution makes an advance payment of part of the invoice value to the supplier.

Payment on due date

When invoices reach their due date, the customer makes full payment of the amount to the financier or directly to the supplier, as previously agreed.

Closure of the operation

Once payment is completed, the risk-based transaction is finalized, settling all obligations between the parties involved.

Risk taken: what is the role of financial institutions?

In the context of factoring , financial institutions play a very important role. They act as intermediaries in the transaction, enabling the anticipation of receivables.

Essentially, as we have seen, they purchase the rights to receive payment from a company that supplies products or services, paying in advance the amount that would be settled on a future date.

For companies operating in the market, especially in the retail sector, this service offered by banks can be extremely beneficial. Through factoring, they can improve cash flow, since they do not need to wait for the payment deadline normally stipulated in commercial transactions.

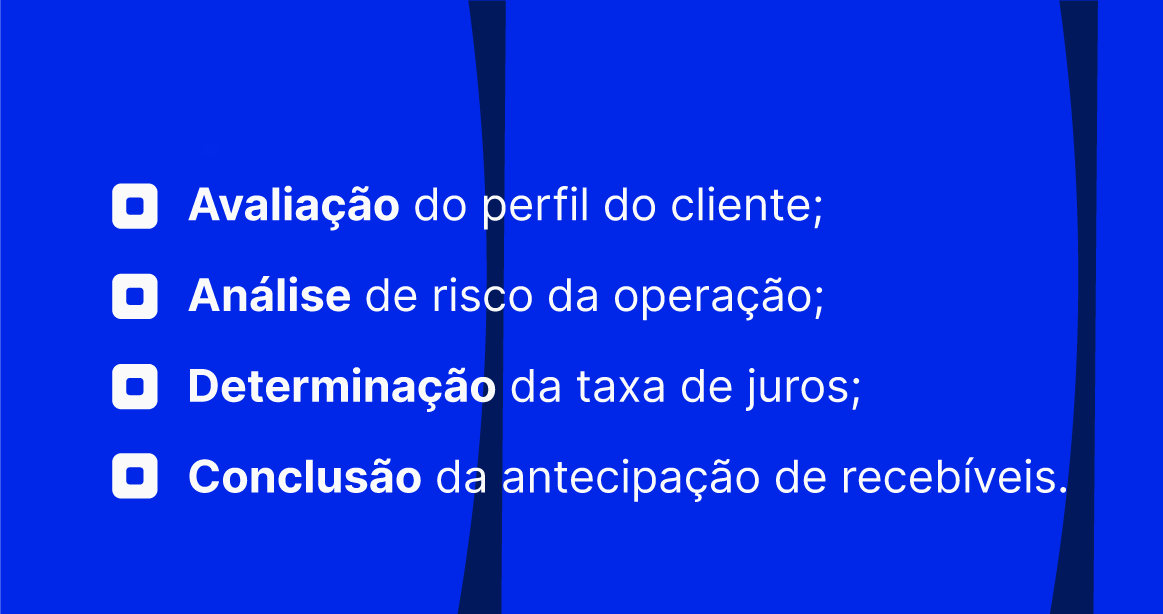

Banks and financial institutions assess the risk of the transaction before proceeding, determining the interest rate to be charged based on the client's profile. The rate will reflect the risk of default, as well as the term of the advance. Thus, it is the responsibility of the financial institution to:

These points show that financial institutions are key players in facilitating access to working capital, which, in turn, allows companies greater capacity for financial planning and investment in their operations.

In this way, factoring operations contribute significantly to boosting the market, offering flexibility so that companies can better manage their payments and receipts.

What are the main advantages of the risk-sharing agreement?

The discounted risk offers several advantages both for companies that choose this type of credit and for their suppliers . Check it out:

For suppliers

In a financial context, factoring represents a valuable tool for suppliers seeking effective and strategic . By adopting this operation, they can navigate the market with greater confidence, taking advantage of the benefits offered and minimizing risks associated with receiving payments.

Here are the main benefits of risk-sharing for this category:

Working capital

The factoring provided offers a significant increase in working capital. By anticipating receivables, suppliers obtain immediate cash flow for their daily operations, without having to wait for the extended payment terms that are normally agreed upon with contractors. This means accessible liquidity that can be quickly reinvested in the market.

- Cash flow: immediate increase;

- Reinvestment : the ability to reinvest in the business quickly.

Tax benefits

Suppliers can access tax benefits associated with factoring operations. In some cases, the anticipation of receivables can result in tax deductions or tax deferral, which constitutes a competitive advantage in the current financial landscape.

- Tax deductions: possibility of reducing the tax burden;

- Tax deferral: an opportunity to postpone tax payments.

Lower risk of default

The risk factor transferred transfers a portion of the default risk to the financial institution that advances the payments. Thus, suppliers mitigate their liquidity risks by ensuring more predictable and secure payment receipts, which can guarantee greater financial stability in a volatile market.

- Risk transfer: to financial institutions.

- Financial stability: predictable and secure payments.

For companies (buyers)

Purchasing companies, by opting for the factoring mechanism, find benefits ranging from better payment terms to the strengthening of commercial relationships. This financial tool directly impacts liquidity and cash flow, in addition to benefiting the entire supply chain. See:

Better trading conditions

Purchasing companies that utilize factoring generally manage to negotiate more flexible payment terms with their suppliers. This is because there is a financial guarantee involved in the transaction, which generates more confidence in the market.

Strengthening trade relations

The adoption of factoring is often interpreted as a sign of credibility and solidity on the part of the purchasing company. This positive perception contributes to the continuous strengthening of the relationship with suppliers.

High liquidity and profitability ratio

By utilizing factoring, companies can improve their liquidity due to the possibility of anticipating receivables, which, consequently, can increase profitability.

Obtaining working capital

The factoring system allows companies to buy now and pay later, which optimizes working capital management without mobilizing a large amount of financial resources.

Cash flow management

With payments spaced further apart, cash flow becomes more predictable and manageable. This allows for effective financial planning and proper allocation of resources.

Supply chain improvement

More attractive rates and conditions on factoring can reduce the total cost of products and services. This has positive impacts on the entire supply chain, from the producer to the end consumer.

Reducing the risk of supply interruption

The practice of factoring minimizes the risk of default and therefore reduces the chances of interruption in the supply of essential products for the company.

Risk taken vs. other forms of financing

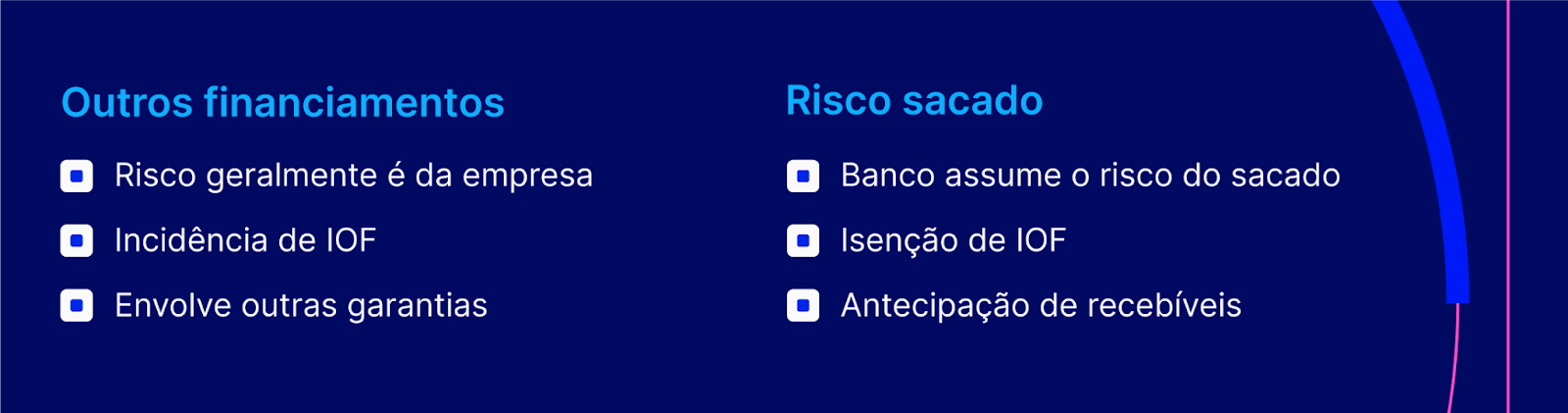

Risk-sharing is a type of financing that has distinct when compared to traditional loans and financing. The main difference lies in the function of the risk: in risk-sharing, the bank or financial institution assumes the credit risk of the drawee , that is, the debtor in relation to the assignor, who is the one who is to receive future credits.

In other forms of financing, such as bank loans and financing, the company taking out the loan bears the full risk , being subject to interest rates based on its ability to pay and credit history. Furthermore, the Financial Operations Tax (IOF) levied on loans and financing increases the total cost for the borrower.

The risk involved is often associated with foreign trade operations known as forfaiting . This practice is attractive for companies that wish to discount export receivables without having to assume the risk of default.

In contrast, loans are more generic and can be used for a variety of purposes, not just in the context of receivables financing.

Retail risk assessment: practicality and advantages

In retail, adopting factoring can simplify financial management while offering tangible benefits for both retailers and their suppliers. Check it out:

Benefits for retail companies

With the risk factor factored in , retail companies can anticipate future revenues, a move that increases liquidity and enables better short-term planning.

Furthermore, it establishes a more stable relationship with suppliers, as it offers them convenient payment options, which can result in more advantageous negotiations for the retailer.

Impact on the supply chain

By opting for factoring, suppliers can anticipate receiving payments and thus manage their cash flow more efficiently, keeping operations stable.

Thus, business continuity is favored when suppliers have the security of receiving payments in advance, which, in turn, positively impacts the entire supply chain.

Risks and considerations

Before undertaking ventures using the risk-taking method, it is crucial that companies are aware of the risks involved and the necessary measures to mitigate them. See below for some aspects of this topic:

Risks associated with the risk of withdrawal

Despite being an extremely advantageous tool, the risk associated with a debt instrument mainly involves credit risk , where the assignor may face default by the debtor.

This risk is amplified if the transaction lacks a bank guarantee or other form of security. Furthermore, economic fluctuations can affect repayment capacity, increasing exposure to risk.

How to mitigate these risks

To minimize these risks, companies can:

- Seek bank guarantees or credit insurance;

- To carry out a detailed analysis of the credit profile of the debtors;

- Diversify the recipients of credit in order to avoid concentrating risk on a single borrower.

Legal and contractual considerations

In legal and contractual terms, it is essential that companies:

- They must comply with regulations regarding debt instruments;

- Draft clear contracts , specifying the terms of the risk involved;

- Include clauses that detail the responsibilities of all parties involved.

What will the new accounting standard for discounted risk be?

The risk-taking mechanism is an accounting practice that gained even more prominence after the inconsistencies in the Americanas case in early 2023. Therefore, it is a tool that is under new regulation.

The International Accounting Standards Board (IASB) has established that, starting in 2024, there will be new rules for the treatment of these transactions in companies' financial statements.

The new accounting standard will stipulate that risk-based transactions must be explicitly detailed in the balance sheet. This will lead to greater transparency and a more faithful representation of the liabilities and assets involved.

Specifically, the rule requires:

- Clear identification of financing operations with suppliers;

- Disclosure of the nature and terms of the transactions;

- The impact of operations on the company's balance sheet and financial health.

In summary, the regulatory change aims to mitigate risks associated with these operations, ensuring that investors and stakeholders can better assess the risks involved in corporate financing. The financial market has reacted positively to this change, expecting greater transparency in corporate accounting practices.

Risk assessed: future trends

Given the recent challenges in the financial market, trends in factoring point towards greater transparency and rigor in accounting. As we have seen, from 2024 onwards, significant changes are expected in the accounting treatment of factoring, directly influencing companies' balance sheets.

These accounting projections are aligned with global efforts to standardize financial practices and increase the reliability of financial reporting.

With these regulations, companies will need to adapt to meet the new requirements. This includes improving the disclosure processes for their risk-draft operations in annual financial statements.

Consequently, these practices may affect how working capital is managed, since factoring is frequently used as a financing mechanism.

In summary, companies should pay attention to the following topics:

- Investments in the development of internal systems;

- Training professionals for the new standards;

- Anticipating the impacts on financial operations.

It is expected that, with these changes, the financial market will gain robustness and risk-based operations will become more transparent, contributing to economic stability and predictability.

Thus, the trend is that such changes will not only protect investors, but also encourage new investments by creating an environment of greater confidence and financial security.

Discover the Skyone marketplace

Now that you know how risk-taking works and are aware of the advantages of this powerful financial practice, you need to learn about the Skyone !

Our platform allows debtors , suppliers , and financial institutions to interact in a secure environment capable of handling high transaction volumes. We automate all manual work, enabling the full anticipation of receivables for your suppliers!

Furthermore, the portal acts as a connection point between anchor companies and their suppliers, providing a complete overview of financial operations and opportunities for receivables financing.

Learn more about our platform and find out how it can benefit your business financially!

Conclusion

As we have seen throughout the article, companies that implement risk-based financing tend to experience more efficient financial management , considering that this practice can offer an important source of resources to maintain financial health and liquidity.

Furthermore, the factoring operation provides reliability in the relationship between suppliers and buyers, since financial institutions are involved to guarantee payment.

Therefore, a thorough understanding of the aspects that make up the risk involved is an essential step in making sound and responsible financial decisions.

Take advantage of this opportunity and complement your learning journey by discovering 5 strategies for anticipating receivables to maintain the health of your cash flow !

Start transforming your company

Test the platform or schedule a conversation with our experts to understand how Skyone can accelerate your digital strategy.